Landscape Assessment of State-Level Climate Financing Options

Introduction

As a response to the climate crisis, India has been progressively introducing policies both at the state and national levels to boost the clean energy sector in India. In 2014, the Government of India embarked on an ambitious plan to increase the share of renewable energy in the country’s energy mix, setting targets to achieve 175 GW of installed renewable energy capacity by 2022. This includes generation of 5 GW of small hydropower, 10 GW of waste-to-energy power, 60 GW of wind power and 100 GW of solar power by 2022. With all the ambitious targets in place, the two major aspects required to transform India’s economy into a green economy include building capacity for increasing both foreign and domestic financial investment and ensuring innovation in its distribution.

We share here the key findings from a report that delves in to the financing aspects of clean energy projects in India with the help of substantial evidence and examples. Based on a primary survey of financial institutions such as banks and non-banking financial institutions (NBFC’s), the report sheds light on policies and financial instruments for renewable energy projects in India.

This weADAPT article is an abridged version of the original text, which can be downloaded from the right-hand column. Please access the original text for more detail, research purposes, full references, or to quote text.

Methodology

15 semi-structured interviews were conducted with stakeholders that included representatives of multilateral development banks, non-banking financial institutions, bilateral agencies, commercial banks, development financial institutions, private equity investors, project developers and civil society institutions. Figure 1 presents a breakdown of stakeholders interviewed. Secondary data was sourced from existing databases including Climate Funds Update, World Bank, ADB, EIB and UNFCCC that track existing initiatives. Literature from national and international institutions obtained from Central and State government programs and schemes was also included. Other sources included International Finance annual reports, Mercom India news reports, reports from Climate Bonds Initiative, Yes Bank reports and the Climate Fund Inventory Database of OECD.

Barriers Associated with Private Sources of Financing

Financial schemes within India’s state and national clean energy policies have been in the form of accelerated depreciation benefits, generation-based schemes, viability gap funding, feed-in tariffs, net metering and tax duty exemptions (IFRI, 2018). In the state of Andhra Pradesh, which is one of the leading states in renewable energy generation, energy policy schemes have been in the form of tax and duty exemptions and favourable transmission charges.

While the growth in solar power has been driven by increasing policy competitiveness of government policies,there still exists several barriers to the financing of clean energy projects in India.

Some of the key challenges are:

- Strong dependence on debt: Private and public sector banks depend mostly on debt sources of financing. This is anticipated to become a critical concern because banks have a certain limit for loans in the infrastructure sector. If they overstretch their lending capacity in one sector, it may in return restrict their possibility of funding to other priority sectors. As estimated by IFRI (2018), as banks move close to their lending limits, their expected ability to provide debt is likely to be reduced by USD 85 billion or 64% of the total expected debt.

- Unfavourable borrowing terms: Though India has access to abundant sources for the generation of renewable energy, unfavourable terms of financing render loans expensive.

- Operational inefficiencies: There is a significant amount of transmission and distribution losses which pose a considerable cost to developers. These losses consist of

- technical losses (which may be due to ill maintained equipment, sub-stations and inadequate investment in infrastructure) and commercial losses (may be due to low metering efficiency, faulty meter reading, theft and pilferages). There are also concerns related to the quality of solar panels from lack of quality control standards.

- Issues with land acquisition : Land acquisition for energy developments is challenging. According to a TERI (2017) study, it takes approximately 6-9 months to procure land for renewable energy purposes. This is compounded by the lack of digitization of land records which makes the process even more cumbersome.

- Information on financial access and disbursement: Recipients are frequently not informed about the sources of funds and the processes to avail them. Hence information asymmetry is one of the key reasons why funds remain unutilised.

- Other risks: In addition to the above factors, there are several risks and uncertainties related to the renewable energy sector in general such as policy and regulatory risks, operational, project development, technological and financing risks.

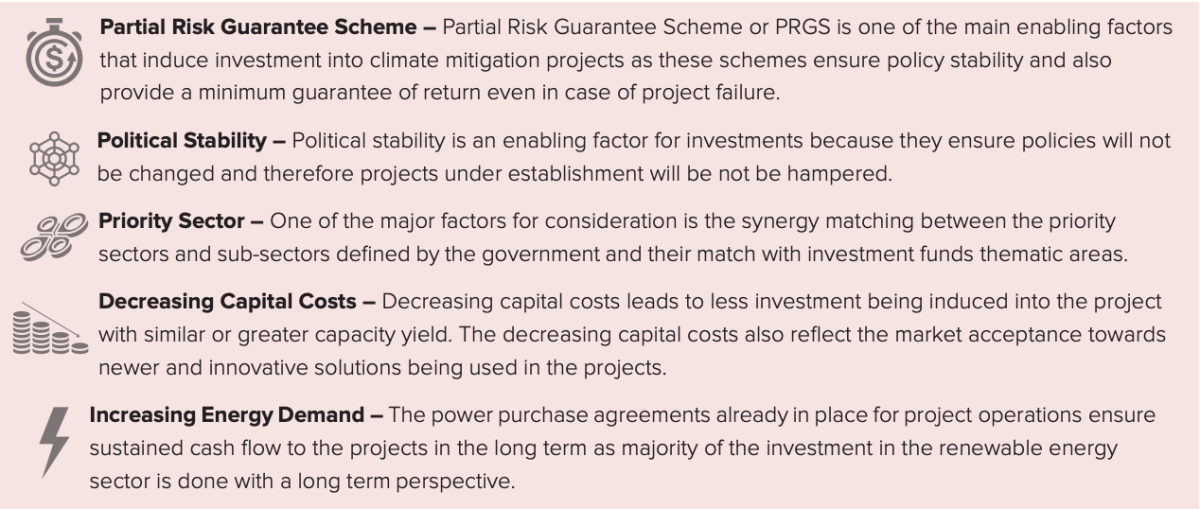

Enabling Factors for the Development of Clean Energy Projects in India

There are a range of enabling factors that can help overcome the identified barriers which are as follows:

Policy Recommendations

Policy recommendations outlined under this report are as follows:

• Capital gains exemption on investment in renewable energy projects through bonds, debt and equity will create huge incentives for both domestic as well as foreign investors.

• Grid charge exemptions to open access solar projects will boost domestic investor confidence and the number of rooftop and small capacity solar projects.

• Creating a single clearance mechanism as against multiple clearances for initiation of renewable energy projects will improve project efficiency.

• Creating a minimum standard of benchmark for PV panels which will improve the overall quality of PV panels being used in the projects and will increase the yield as well as the duration of the project.

• Facilitating power-delivery contracts signed in foreign currencies will allow the project developer to repay debt faster and without the hassle of converting the amount from resident or local currency into foreign currency.

• Improve the monitoring mechanism under the National Clean Energy and Environment Fund (NCEEF) to improve efficient utilization of the funds.

Suggested Citation:

Development Alternatives. (2020).“Landscape assessment of state-level climate financing options”.https://devalt.org/images/L2_ProjectPdfs/SSEFReport-0204.pdf?Oid=275

Further Reading:

Related resources

- Financing Inclusive Low-Carbon Resilient Development: The Role of the Alternative Energy Promotion Centre in Nepal

- Financing transboundary water investments – from public good to shared interest

- Engaging the private sector in financing adaptation to climate change: Learning from practice

- Climate finance: is it making a difference? A review of the effectiveness of multilateral climate funds

(0) Comments

There is no content